AFTER just 18 days as Deutsche Bank’s chief executive, Christian Sewing had two tasks to perform on April 26th. The easy one, inherited from his ousted predecessor, John Cryan, was to

report predictably glum first-quarter results. Net profit dropped by 79%, year on year, to only €120m ($147m). Harder was indicating where he might lead Germany’s troubled leading lender. The rough answer is: back towards Europe, and away from any aspiration to be a global investment bank.

Mr Sewing intends to concentrate more on raising finance and managing payments and currencies for big European companies, and less on America and Asia. He plans to cut the small swaps-repurchasing business in America and to focus the buying and selling of shares for hedge funds and other investors on the most profitable clients. By 2021 corporate and investment banking’s share of total revenues will be trimmed to 50%, from 54% last year. As a result, Mr Sewing said, earnings should become more stable.

Upgrade your inbox and get our Daily Dispatch and Editor's Picks.

Latest stories

What is the Singularity?

China and Eurovision clash over an LGBT performance—and the value of diversity

Can coach companies lure business people on board?

Partisanship at Eurovision is becoming more blatant

Bavaria is the latest place where the church and Christian politicians are at odds

“Cold War” is a faultless romantic epic

So far, says Andrew Coombs of Citigroup, Mr Sewing has supplied “more questions than answers”. He thundered about cost-cutting. Yet he still aims only to keep operating costs below €23bn this year—a target raised by €1bn in February. Longer-term guidance for costs, revenue, assets and leverage is still to come. Mr Coombs worries that restructuring may cost far more than Deutsche is allowing for. So the leverage ratio (a gauge of capital strength), which at 3.7% is well below the figures for its peers, may fall in the short run. Withdrawal from those trading businesses should lift it, but because contracts can last a long time, this may take a while.

As well as its corporate and investment bank, Deutsche has Germany’s biggest retail bank (plus banks in Italy and Spain) and an asset manager, DWS. It thus seems to be settling for being a universal bank with its centre of gravity in Europe. This is far from the course of the 1990s and 2000s, when Deutsche and other European adventurers took on Wall Street.

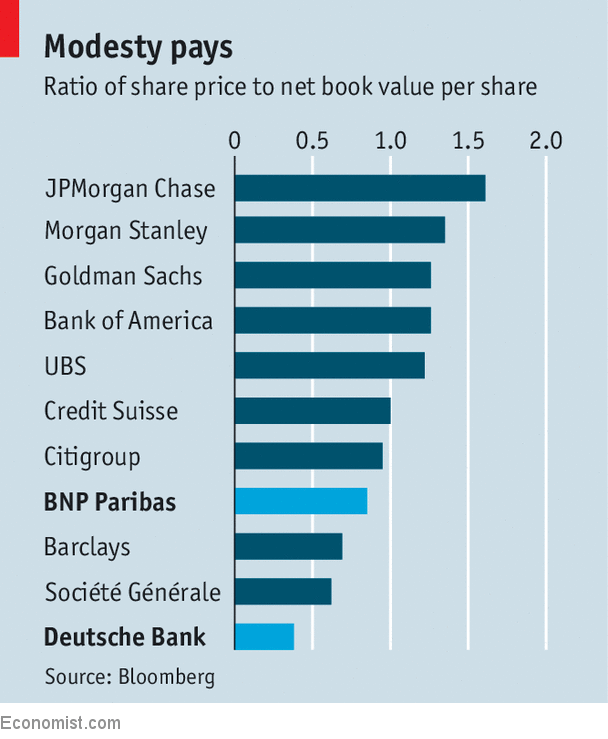

Such a model can be made to pay. France’s BNP Paribas also combines retail banking, in Belgium, Italy and Luxembourg as well as at home, with a division serving corporations and institutional investors that has a strong European flavour. Granted, the French bank, which is due to report first-quarter results on May 4th, returned an unspectacular 8.9% on equity last year (it hopes for 10%-plus by 2020). Its stockmarket worth is 15% below the book value of its assets. But for Deutsche, that’s dreamland (see chart).

There are important differences. France has a few big banks; Germany lots of small ones. Though bigger by assets than Deutsche, BNP Paribas is a smaller investment bank. Coalition, a research firm, ranks it sixth in Europe and Deutsche second, with Americans taking the other top slots.

Come what may, Europeans’ glory days are gone. Tighter capital rules since the financial crisis, notes Alastair Ryan of Bank of America Merrill Lynch, have hit them harder than American banks. The Americans’ vast balance-sheets and huge domestic market give them scale that Europeans, with smaller markets and minuscule rates and margins, cannot match.

The Americans were also quicker than Europeans to shape up after the crisis. Europeans have had to choose new models. Switzerland’s UBS tacked from investment banking towards wealth management; Credit Suisse may have pivoted to Asia just in time; Barclays styles itself as a transatlantic bank; BNP Paribas was never a true swashbuckler anyway.

Even by European standards, Deutsche was slow. As late as 2015 it believed that as others retrenched it would be the “last man standing” and make a killing when business picked up. Did it wake up too late? Over to you, Mr Sewing.